Creating One of the Largest Gold Development Companies in the

United States with an Enhanced Platform for Heap Leach Gold

Production from Low CapEx Brownfield Sites

NOT FOR DISTRIBUTION TO UNITED STATES NEWS WIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

TORONTO, April 10, 2024 (GLOBE NEWSWIRE) -- Reviva l Gold Inc. (TSXV: RVG, OTCQX: RVLGF) (“Revival Gold” or the “Company”) is pleased to announce that it has entered into a definitive business combination agreement with Ensign Minerals Inc. (“Ensign”) and Revival Gold Amalgamation Corp. (“Revival Subco”) dated April 9 th , 2024 (the “Definitive Agreement”), whereby Revival Gold will acquire all of the issued and outstanding shares of Ensign, a private company, in exchange for an aggregate of 61,376,126 million shares of Revival Gold based on a share exchange ratio of 1.1667 Revival shares for each Ensign share. Upon completion of the proposed business combination (the “Transaction”), Revival Gold will pursue engineering and economic studies at the newly acquired Mercur Gold Project (“Mercur”) located in Utah, USA while continuing to advance permitting preparations and ongoing exploration at the Company’s Beartrack-Arnett Gold Project (“Beartrack-Arnett”) located in Idaho, USA.

In connection with the Transaction, Paradigm Capital Inc. and BMO Capital Markets Inc. have agreed to act as lead agents and joint bookrunners, on behalf of a syndicate of agents, in connection with a concurrent offering of subscription receipts of Revival Subco (the “Subscription Receipts”) for aggregate gross proceeds of C$7,000,000 (the “Concurrent Offering”).

Transaction Highlights

-

Delivers Accretive Growth.

With aggregate Measured and Indicated Mineral Resources of 2.4 million ounces of gold

1

,3

and Inferred Mineral Resources of 3.8 million ounces of gold

2,3

, the Transaction increases Revival Gold’s heap leach gold resources per share and creates one of the largest, pure gold, development companies in the United States

4

.

-

Shortens Estimated Timeline to Heap Leach Gold Production

. Mercur’s preferential location on predominately patented (private) claims, in a semi-arid zone, with existing infrastructure, and a short drive from Salt Lake City, Utah, is ideal for permitting and is expected to accelerate Revival Gold’s goal of becoming a mid-tier U.S. heap leach gold producer.

-

Complementary and Sizeable Asset Base

. Opportunity for capital efficient phased production growth from brownfield sites with a combined target open pit heap leach production objective of 150,000 ounces of gold per year from Mercur and Beartrack-Arnett, potentially growing to greater than 250,000 ounces of gold per year with the exploitation of Beartrack-Arnett underground mill material.

5,6

A phased development approach lowers risk and creates greater value per share as the business grows.

-

Significant Exploration Potential

. Numerous open exploration targets have been identified on the extensive land packages at both Mercur in the northeastern Great Basin and Beartrack-Arnett in the Idaho Orogenic Gold Belt.

-

Synergies

. The regional proximity of the projects offers the potential to unlock management, G&A, operational and public market efficiencies. No significant additional management resources are required since the assets are in adjacent states approximately six hours’ drive from each other. There is potential to leverage cross-project experience and expertise to collaborate on studies, permitting, and project de-risking.

-

Financial Strength

. Concurrent C$7 million equity financing and existing cash balances will provide funding support to advance key milestones at Mercur and Beartrack-Arnett.

-

Veteran Leadership in Gold.

The resulting company will have significant in-state experience in the exploration, development, and operation of gold projects in the Western U.S. with strategic and capital markets leadership from Toronto backed by a larger group of key shareholders.

Notes: 1 Contained within 86.2 million tonnes at 0.87 g/t gold at Beartrack-Arnett. 2 Contained within 50.7 million tonnes at 1.34 g/t gold at Beartrack-Arnett for 2.19 million ounces of gold and 89.6 million tonnes at 0.57 g/t gold at Mercur for 1.64 million ounces of gold. 3 See “Preliminary Feasibility Study NI 43-101 Technical Report on the Beartrack-Arnett Heap Leach Project, Lemhi County, Idaho, USA” prepared by Kappes, Cassidy & Associates, IMC, KCH and WSP, dated August 2 nd , 2023, and “NI 43-101 Technical Report for the Mercur Project, Camp Floyd and Ophir Mining Districts, Tooele & Utah Counties, Utah, USA” prepared by Lions Gate Geological Consulting Inc., RESPEC Company LLC, and Kappes, Cassidy & Associates, dated February 1 st , 2024, for further details. 4 Based on analysis of industry peers, pre and post transaction Revival Gold shares outstanding, and pro-forma Mineral Resources noted in the Technical Reports referenced above. 5 Target production based on Beartrack-Arnett 2023 PFS average production and future potential from Mercur Mineral Resource. 6 Considers potential underground operation for Beartrack-Arnett based PFS Mineral Resource factors including 2,500 tpd unground throughput, average grade, and recovery.

"With the addition of Mercur, we expect to shorten our estimated timeline to heap leach gold production while increasing the potential production scale of Revival Gold’s heap leach gold business to approximately 150,000 ounces per year. The combined Mineral Resource will vault Revival Gold ahead to become one of the largest, pure gold, development companies in the United States”, said Revival Gold President & CEO, Hugh Agro.

Mr. Agro further commented: “We are pleased to be entrusted by Ensign’s shareholders with the future development of Mercur. The Transaction is a “win-win” outcome for all concerned creating a clear path for Revival Gold to unlock significant value for shareholders by potentially expediting the path to become a mid-tier open pit heap leach gold producer. With Mercur, Revival Gold will obtain a high-quality complementary project at an attractive acquisition price of about US$10 per ounce in situ . Incorporating an asset that brings forward Revival Gold’s potential production date marks a considerable enhancement to the value, risk profile, and upside for the Company”.

John Knowles, Chairman and Director of Ensign, added: “Ensign is pleased to join with Revival Gold to deliver value for our respective shareholders in gold. The combined company will feature veteran industry leadership, synergistic and complementary gold assets, and a credible business plan to become a cash-flowing mid-tier U.S. gold producer”.

Conference Call

Management will host a conference call later this morning to discuss Revival Gold’s acquisition of Ensign.

Call-in information below:

| Scheduled Start: | Wednesday, April 10 th , 2024, 10:00 am EST |

| Call-In Number: | 416-764-8658 |

| Toll-Free in North America: | 888-886-7786 |

A replay of the conference call will be available for one week at 416-764-8691 or toll-free in North America at 877-674-6060. Playback passcode 712425#.

Transaction Details

Pursuant to the terms of the Definitive Agreement, Revival Gold will acquire all of the issued and outstanding common shares of Ensign pursuant to a statutory three-cornered amalgamation (the “Amalgamation”) under the Business Corporations Act (British Columbia), whereby Ensign and Revival Gold Amalgamation Corp., a wholly-owned subsidiary of Revival Gold incorporated for the purpose of completing the Amalgamation, will amalgamate to form a newly amalgamated company (“Amalco”). Under the Amalgamation, shareholders of Ensign (“Ensign Shareholders”), other than Ensign Shareholders who have validly exercised and have not withdrawn rights of dissent, will receive 1.1667 Revival Shares (as defined below) for each one common share of Ensign (each, an “Ensign Share”) held. The consideration implies a purchase price of C$0.4164 per Ensign Share, or gross consideration of approximately C$21.9 million, based on a deemed 20-day volume weighted average price per Revival Share of C$0.3569 prior to announcement. Upon completion of the Amalgamation, Amalco will become a wholly owned subsidiary of Revival Gold. As of the date hereof, there are (i) 113,159,547 Revival Shares issued and outstanding, and (ii) 52,606,605 Ensign Shares issued and outstanding. Upon completion of the Transaction (and without accounting for the Concurrent Offering), Revival Gold is expected to have approximately 174,535,673 Revival Shares issued and outstanding, on an undiluted basis, with (i) approximately 65% of such Revival Shares expected to be held by the current shareholders of Revival Gold, and (ii) approximately 35% of such Revival Shares expected to be held by the former shareholders of Ensign.

Upon completion of the Transaction, Revival Gold will be the parent company and the sole shareholder of Amalco and will indirectly carry on the current business of Ensign. In connection with the Transaction, Ensign will seek the approval of its shareholders with respect to the Amalgamation at a meeting of Ensign Shareholders to be convened around the end of April 2024 (the “Ensign Meeting”). An information circular providing further information on the Amalgamation will be provided to the Ensign Shareholders in connection with the Ensign Meeting.

The Transaction has been unanimously approved by the Boards of Directors of Revival Gold and Ensign, and the Board of Directors of Ensign recommends that Ensign shareholders vote in favour of the Transaction and related matters. Ensign’s Board and management and other shareholders representing approximately 27% of the Ensign Shares have entered into voting support agreements in support of the transaction. Wayne Hubert, Revival Gold’s current Non-Executive Chairman, is the President and CEO and a Director of Ensign and abstained from voting on the Transaction for both Revival Gold and Ensign due to conflicting interests. Closing of the Transaction is subject to certain condition precedents, including but not limited to: Obtaining Ensign Shareholder approval at the Ensign Meeting, obtaining any applicable regulatory approvals including the approval of the TSXV, closing of the Concurrent Offering for aggregate gross proceeds of a minimum of $5,000,000, and other customary conditions for transactions of this nature.

The Board of Directors of Revival Gold has received an opinion from MPA Morrison Park Advisors Inc. to the effect that, based on and subject to the assumptions, limitations, and qualifications stated in such opinion, the consideration to be paid by Revival Gold pursuant to the Transaction is fair, from a financial point of view to Revival Gold.

The Board of Directors of Revival Gold following the closing of the Transaction is expected to remain at seven (7) Directors, with Ensign Board of Director nominee Norm Pitcher expected to replace Michael Mansfield as a Director of Revival Gold, who is expected to resign from his position upon closing of the Transaction. Additionally, upon closing of the Transaction, Revival Gold expects to designate independent Director Tim Warman as Non-Executive Chairman, with Hugh Agro serving as President & CEO and Director, John Meyer as Vice President, Engineering & Development, and Lisa Ross as Vice President & CFO.

Mercur Gold Project Overview

The majority of the information summarized below on Mercur has been extracted from the Technical Report titled, “NI 43-101 Technical Report for the Mercur Project, Camp Floyd and Ophir Mining Districts, Tooele & Utah Counties, Utah, USA”, prepared by Lions Gate Geological Consulting Inc., RESPEC Company LLC, and Kappes, Cassidy & Associates, dated February 1 st , 2024. The Technical Report will be filed within 45 days of this news release under Revival Gold’s SEDAR+ profile (www.sedarplus.ca). Readers are encouraged to read this technical report in its entirety, including all qualifications, assumptions and exclusions that relate to the Mineral Resource estimate. This technical report is intended to be read as a whole, and sections should not be read or relied upon out of context.

1.

Location and History

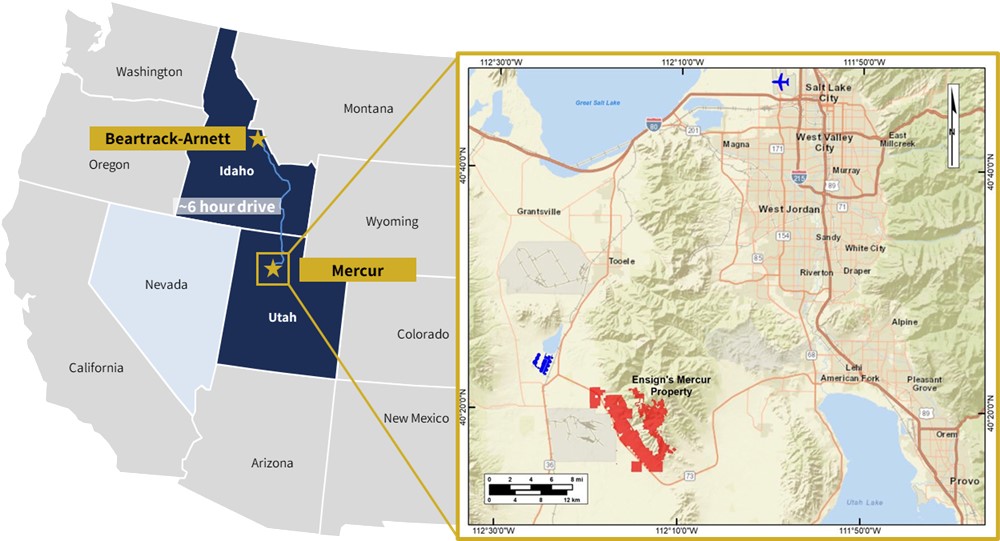

Mercur is located 57 kilometers southwest of Salt Lake City in the Oquirrh Mountains in Utah, a highly mineralized mountain range that is also host to the Barney’s Canyon and Melco sediment-hosted gold deposits, and Bingham Canyon, one of the world’s largest copper-gold mines. See Figure 1, Location Map, below.

Figure 1: Mercur Gold Project Location Map

Historically, 2.6 million ounces of gold were mined from the Mercur District, including approximately 1.5 million ounces of gold produced from Mercur by Getty Oil Company (“Getty”) and later Barrick Gold (“Barrick”) during the period of 1983 to 1998.

Mercur includes interests in 463 patented mining claims, 426 fee land tax parcels, 395 unpatented lode mining claims, three unpatented mill site claims, and six Utah state metalliferous minerals leases that cover 6,255 net hectares (approximately 15,300 net acres) of mineral rights. The existing Mineral Resources are primarily situated on private land.

Barrick operated Mercur until 1998 when it was closed due to low gold prices. Since closure, Barrick has substantially completed reclamation of the Mercur site.

In August 2020, Ensign executed an assignment agreement with Rush Valley Exploration for 3,579 net hectares primarily in the West Mercur area, which was followed by, also in August 2020, a merger agreement with Priority Minerals securing an additional 213 net hectares in the South Mercur area.

On May 13, 2021, Ensign entered into an option agreement (subsequently amended on June 13, 2022, May 15, 2023, and April 1, 2024) with Barrick (the “Barrick Agreement”) to acquire Barrick’s interests in the Mercur area (the “Mercur Option”). The Barrick Agreement, as amended, which has an expiry of January 2, 2026, enables Ensign to acquire Barrick’s interests for a total of US$20 million in cash or, at the sole discretion of Barrick, shares, payable as follows:

| (i) | US$5 million due on exercise of the Mercur Option; |

| (ii) | US$5 million due on first anniversary of commercial production at Mercur; |

| (iii) | US$5 million due on second anniversary of commercial production at Mercur; and, |

| (iv) | US$5 million due on third anniversary of commercial production at Mercur. |

In addition, in connection with the Barrick Agreement, Ensign issued Barrick four million Ensign warrants with an exercise price of C$0.25 per Ensign share and an expiry of January 2, 2029, and granted Barrick a 2% Net Smelter Return (“NSR”) over the Main Mercur area and a 1% Area of Interest NSR over certain other Barrick claims within the Mercur district.

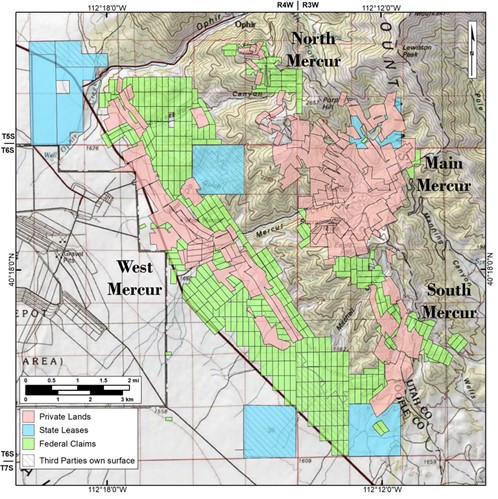

In late August 2021, Ensign completed an option and assignment agreement with Mountainwest Minerals for certain claims in South Mercur. In October 2021, two option and assignment agreements were executed with Sacramento Gold Mining (three-year option to explore 90 net hectares) and Geyser Marion Gold Mining (three-year option to explore 673 net hectares). Throughout 2021, Ensign staked several claims at Main, North, South and West Mercur. In 2022, Ensign executed an exploration license with an option to purchase on one claim held by a private party and purchased a 4.2% outstanding interest on some of its properties to consolidate a 100% interest. In 2023, Ensign leased an outstanding 25% interest in certain claims to increase its interest to 75%. The resulting Mercur property position is outlined in Figure 2, Mercur Gold Project Claim Map, below.

Figure 2: Mercur Gold Project Claim Map

2.

Mineral Resource and Geology

The Mercur property hosts an Inferred Mineral Resource of 89.6 million tonnes, grading 0.57 g/t gold containing 1.64 million ounces of gold as summarized in Table 1, Mercur Gold Project Mineral Resource, below.

Table 1: Mercur Gold Project Mineral Resource Estimate

| Deposit |

Tonnes

(Mt) |

Gold

(g/t) |

Contained Gold

(koz) |

| Main Mercur | 74.1 | 0.57 | 1,350 |

| South Mercur | 15.6 | 0.59 | 290 |

| Total Inferred | 89.6 | 0.57 | 1,640 |

Note: See “NI 43-101 Technical Report for the Mercur Project, Camp Floyd and Ophir Mining Districts, Tooele & Utah Counties, Utah, USA” prepared by Lions Gate Geological Consulting Inc., RESPEC Company LLC, and Kappes, Cassidy & Associates, dated February 1st, 2024, for further details.

The Mercur Mineral Resource has been estimated in conformity with generally accepted guidelines outlined in CIM Estimation of Mineral Resources and Mineral Reserves Best Practices Guidelines (November 29, 2019) and is reported in accordance with NI 43-101.

Estimations are made from 3D block models based on geostatistical applications using commercial mine planning software (MinePlan). The project limits are based on a local mine grid system. Separate block models were set up for Main Mercur and South Mercur with a nominal block size of 50 x 50 x 30 feet (15 x 15 x 9 meters). Sample data is derived from a combination of surface diamond and reverse circulation drill holes. The pierce points of the drill holes into the mineralized zone vary but can be approximately 25- to 50-foot (8- to 15-meter) spacing in the areas of historic mining.

There is a total of 2,970 drillholes in the block models. Of these, 2,861 holes are historical holes that were primarily drilled by Barrick and Getty, and 109 holes were drilled by Ensign. Comparisons show that the Ensign drill hole and Barrick drill hole sample results agree over all areas being investigated.

The Mercur Mineral Resource estimate has been generated from drill hole sample assay results and the interpretation of a geologic model that relates to the spatial distribution of gold and silver. Interpolation characteristics were defined based on the geology, drill hole spacing, and geostatistical analysis of the data. The Mineral Resources were classified according to their proximity to sample data locations and are reported, as required by NI 43-101, according to the CIM Definition Standards for Mineral Resources and Mineral Reserves (May 2014).

3.

Exploration & Development

Revival Gold considers the large regional package at Mercur to hold attractive potential for additional discoveries based on the project’s track record of past production and the results of recent fieldwork undertaken by Ensign. Nevertheless, Revival Gold’s primary objective with its work programs on Mercur over the next 6-12 months will be to advance metallurgy, optimize the project’s geological model and pursue the completion of a potential PEA.

While advancing towards a PEA, Revival Gold expects to continue the compilation of historical data, property-wide prospecting, geological mapping, and planning for potential future exploration drilling.

The potential exists to expand existing resources and to identify new gold resources beyond the pit margins of the historical Mercur mine. At South Mercur, there are also opportunities to expand the known gold mineralization.

In addition to the potential expansion of known mineralization at Main Mercur and South Mercur, Mercur offers several exploration opportunities for new targets. At Main Mercur, the potential for mineralized feeder structures and deeper, potential stratigraphic host units is under-explored. At South Mercur, where mineralization seems to occur at the intersection of the northerly striking Mercur Member beds and northwest-trending structural zones, there is potential for the discovery of new en-echelon pods of mineralization. The West Mercur pediment is a greenfield area that holds potential for deposits concealed beneath relatively thin alluvial cover. North Mercur is an early-stage exploration area that has permissive geology for new silver and gold discoveries.

4.

Metallurgy

Mineralization at Mercur consists of very fine to fine gold particles associated with oxide, sulfide, and carbonaceous minerals. The oxidation profile in the deposits is complex with influence from bottom-up fluid movement and structural disruption. A carbon-in-leach (“CIL”) process plant was built and commissioned at the site in 1983 to process the higher-grade ore and operated until 1997. This CIL plant operated until 1997 and produced approximately 1.5 million ounces of gold. A dump heap leach for the low-grade materials operated from 1985 to 1998 producing approximately 380,000 ounces of gold. In 1988, a pressure oxidation (“POX”) plant was installed to treat refractory sulfide materials. This POX plant operated until February 1996 and pre-processed approximately 300,000 ounces of gold ultimately produced out of the CIL plant. Mercur produced approximately 1.5 million ounces of gold until it was closed by Barrick in 1998.

Ensign’s focus has been on potential heap leachable and/or CIL material at Mercur. During 2022 and 2023, initial metallurgical test work was completed for Ensign jointly by Bureau Veritas Minerals in Richmond, British Columbia, Canada and ALS Metallurgy in Kamloops, British Columbia, Canada. This work included ten CIL bottle roll cyanide amenability tests (2022) and ten direct cyanidation (“DCN”) leach tests (2022).

Historical and Ensign DCN testing results were used by Ensign’s consultants to estimate heap leach gold recoveries. DCN estimates were incorporated into the Mercur block model then discounted by 15% to reflect potential heap leach gold recoveries. The gold recoveries assumed for the Mercur Mineral Resource estimate by domain are summarized in Table 2 below.

Table 2: Heap Leach Gold Recoveries Assumed for the Mercur Mineral Resource

| Mineral Resource Area |

Tonnes

(Mt) |

Estimated Heap Leach

Gold Recovery |

| Main Mercur | 74.1 | 65% |

| South Mercur | 15.6 | 55% |

| Total/Weighted Average | 89.6 | 63 % |

Note: See “NI 43-101 Technical Report for the Mercur Project, Camp Floyd and Ophir Mining Districts, Tooele & Utah Counties, Utah, USA” prepared by Lions Gate Geological Consulting Inc., RESPEC Company LLC, and Kappes, Cassidy & Associates, dated February 1st, 2024, for further details.

5.

Existing Infrastructure

Mercur has existing infrastructure with a paved access road to the Mercur security gate. The former Barrick mine offices and security gate are operational. The site is connected to grid power at 460 kW and has potential access to water through wells used by the prior operation. The wells and associated water rights are currently held by Tooele County and are not in use.

Concurrent Offering Details

Revival Gold will issue a subsequent news release outlining the details of the proposed Concurrent Offering once finalized. The net proceeds of the Concurrent Offering are expected to be used by Revival Gold, following completion of the Transaction, to complete a Preliminary Economic Assessment (“PEA”) on Mercur, advance permitting preparations on Beartrack-Arnett, continue exploration for high-grade material at Beartrack-Arnett, and for working capital and general corporate purposes. In addition, Revival Gold will grant the Agents an option, exercisable, in whole or in part, for a period of up to two (2) business days prior to the closing of the Concurrent Offering, to sell up to an additional 15% of the Subscription Receipts offered under the Concurrent Offering. The Concurrent Offering is subject to settling definitive terms, the approval of the TSX Venture Exchange (the “TSXV”) and other necessary regulatory approvals. The Concurrent Offering is expected to close in early May, 2024.

Select Financial Information

The following table presents selected financial statement information with respect to Ensign. Such information is derived from the unaudited financial statements of Ensign for the financial years ended December 31, 2023, and 2022, and the unaudited interim financial statements of Ensign for the nine months ended September 30, 2023.

| As at September 30, 2023 ($US) | As at December 31, 2023 ($US) |

As at December 31, 2022 ($US)

|

|

| Current Assets | 147,788 | 82,012 | 722,056 |

| Non-Current Assets | 4,163,063 | 4,149,430 | 4,339,396 |

| Total Assets | 4,310,851 | 4,231,442 | 5,061,452 |

| Current Liabilities | 35,246 | 361,749 | 13,799 |

| Non-Current Liabilities | - | - | - |

| Total Liabilities | 35,246 | 361,749 | 13,799 |

| Net Assets | 4,275,605 | 3,869,693 | 5,047,653 |

| Nine months ended September 30, 2023 ($US) | Year ended December 31, 2023 ($US) |

Year ended December 31, 2022 ($US)

|

|

| Exploration and Evaluation costs | 697,081 | 931,683 | 3,124,919 |

| Administration and Travel | 453,543 | 606,182 | 1,017,729 |

| Share Based Compensation | 287,940 | 305,026 | 262,253 |

| Other Expenses | 744 | 1,075 | - |

| Depreciation | 44,665 | 58,298 | 61,016 |

| Interest and Financing | 57 | 57 | 465 |

| Net loss for the period | 1,484,030 | 1,902,321 | 4,466,382 |

Since inception, Ensign has issued 52.6 million common shares for consideration totalling C$18.7 million (approximately C$0.36 per Ensign common share) and incurred cumulative exploration expenditures of approximately US$7,500,000.

The securities being offered pursuant to the Concurrent Offering, or the Transaction have not been, nor will they be, registered under the U.S. Securities Act and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons absent registration or an applicable exemption from the registration requirements. This news release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities in any state in which such offer, solicitation or sale would be unlawful. “United States” and “U.S. person” are as defined in Regulation S under the U.S. Securities Act.

Advisors and Counsel

MPA Morrison Park Advisors Inc. is acting as financial advisor to Revival Gold. Peterson McVicar LLP is acting as Revival Gold’s legal counsel. Osler, Hoskin & Harcourt LLP is acting as Ensign’s legal counsel.

Qualified Persons

John P.W. Meyer, Vice President, Engineering and Development, P.Eng., and Steven T. Priesmeyer, C.P.G., Vice President Exploration, Revival Gold Inc., are the Company’s designated Qualified Persons for this news release within the meaning of National Instrument 43-101 Standards of Disclosure for Mineral Projects and have reviewed and approved its scientific and technical content.

About Revival Gold Inc.

Revival Gold is a growth-focused gold exploration and development company. The Company is advancing the Beartrack-Arnett Gold Project located in Idaho, USA.

Beartrack-Arnett is the largest past-producing gold mine in Idaho. The Project benefits from extensive existing infrastructure and is the subject of a recent Preliminary Feasibility Study for the potential restart of open pit heap leach gold production operations.

Since reassembling the Beartrack-Arnett land position in 2017, Revival Gold has made one of the largest new discoveries of gold in the United States in the past decade. The mineralized trend at Beartrack extends for over five kilometers and is open on strike and at depth. Mineralization at Arnett is open in all directions.

Additional disclosure including the Company’s financial statements, technical reports, news releases and other information can be obtained at www.revival-gold.com or on SEDAR+ at www.sedarplus.ca .

For further information, please contact:

Hugh Agro, President or CEO or Lisa Ross, CFO

Telephone: (416) 366-4100 or Email:

info@revival-gold.com

.

Ensign Minerals Inc.

Ensign is a private company existing under the Business Corporations Act (British Columbia) and focused on exploring for precious metals within the Mercur District, Utah, USA. Ensign controls approximately 6,255 hectares in the district where the known mineralization occurs on primarily privately held patented claims. Ensign’s property holdings include Mercur, West Mercur, South Mercur and North Mercur.

Cautionary Statement

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

This press release includes certain "forward-looking information" within the meaning of Canadian securities legislation and “forward-looking statements” within the meaning of U.S. securities legislation (collectively “forward-looking statements”). Forward-looking statements are not comprised of historical facts. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Forward-looking statements may be identified by such terms as “believes”, “anticipates”, “expects”, “estimates”, “may”, “could”, “would”, “will”, or “plan”. Since forward-looking statements are based on assumptions and address future events and conditions, by their very nature they involve inherent risks and uncertainties. Although these statements are based on information currently available to the Company, the Company provides no assurance that actual results will meet management’s expectations. Risks, uncertainties, and other factors involved with forward-looking statements could cause actual events, results, performance, prospects, and opportunities to differ materially from those expressed or implied by such forward-looking statements.

Forward-looking statements in this document include, but are not limited to, the advancement of permitting preparations and ongoing exploration at Beartrack-Arnett, the shortening of Revival Gold’s estimated timing to heap leach gold production, statements with respect to the potential production scale of Revival Gold’s heap leach gold business, the opportunity for capital efficient phased production growth from brownfield sites, a phased development approach lowers risk and creates greater value per share as the business grows, potential synergies between Revival Gold and Ensign, risk factors relating to the timely receipt of all applicable shareholder, regulatory and third party approvals for the Concurrent Offering or the Transaction, including that of the TSX Venture Exchange, that the Concurrent Offering or the Transaction may not close within the timeframe anticipated or at all or may not close on the terms and conditions currently anticipated by the Company for a number of reasons including, without limitation, as a result of the occurrence of a material adverse change, disaster, change of law or other failure to satisfy the conditions to closing of the Offering; the inability of the Company to apply the use of proceeds from the Offering as anticipated; the size of the Concurrent Offering, the resale restrictions of the securities issued pursuant to the Concurrent Offering, the ability of Revival Gold to unlock value for shareholders and enhance the value, risk profile and upside for the Company, Revival Gold having a credible business plan to become a cash-flowing mid-tier U.S. gold producer, the expected timing of the Ensign Meeting, Revival Gold’s primary objective with its work programs on Mercur over the next 6-12 months being to advance metallurgy, optimize the project’s geological model and pursue the completion of a potential PEA, satisfaction of the Escrow Release Conditions, the Company’s objectives, goals and future plans, and statements of intent, the implications of exploration results, mineral resource/reserve estimates and the economic analysis thereof, exploration and mine development plans, timing of the commencement of operations, estimates of market conditions, and statements regarding the results of the pre-feasibility study, including the anticipated capital and operating costs, sustaining costs, net present value, internal rate of return, payback period, process capacity, average annual metal production, average process recoveries, concession renewal, permitting of the project, anticipated mining and processing methods, proposed pre-feasibility study production schedule and metal production profile, anticipated construction period, anticipated mine life, expected recoveries and grades, anticipated production rates, infrastructure, social and environmental impact studies, availability of labour, tax rates and commodity prices that would support development of the Project. Factors that could cause actual results to differ materially from such forward-looking statements include, but are not limited to failure to identify mineral resources, failure to convert estimated mineral resources to reserves, the inability to maintain the modelling and assumptions upon which the interpretation of results are based after further testing, the inability to complete a feasibility study which recommends a production decision, the preliminary nature of metallurgical test results, delays in obtaining or failures to obtain required governmental, environmental or other project approvals, changes in regulatory requirements, political and social risks, uncertainties relating to the availability and costs of financing needed in the future, uncertainties or challenges related to mineral title in the Company’s projects, changes in equity markets, inflation, changes in exchange rates, fluctuations in commodity and in particular gold prices, delays in the development of projects, capital, operating and reclamation costs varying significantly from estimates, the continued availability of capital, accidents and labour disputes, and the other risks involved in the mineral exploration and development industry, an inability to raise additional funding, the manner the Company uses its cash or the proceeds of an offering of the Company’s securities, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, future climatic conditions, the discovery of new, large, low-cost mineral deposits, the general level of global economic activity, disasters or environmental or climatic events which affect the infrastructure on which the project is dependent, and those risks set out in the Company’s public documents filed on SEDAR+. Although the Company believes that the assumptions and factors used in preparing the forward-looking statements in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. Specific reference is made to the most recent Annual Information Form filed on SEDAR+ for a more detailed discussion of some of the factors underlying forward-looking statements and the risks that may affect the Company’s ability to achieve the expectations set forth in the forward-looking statements contained in this presentation. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, other than as required by law.